Thaler’s Research

Richard Thaler introduced mental accounting in Marketing Science (1985) and elaborated the framework in the Journal of Behavioral Decision Making (1999). The core observation: people do not treat all money as equivalent even when it is objectively identical. Windfall money (a bonus, a gift, a tax refund) is spent more freely than earned money of the same amount. “Fun money” and “investment money” are treated as non-interchangeable even when the financial logic of fungibility would dictate treating them identically.

Three properties characterize mental accounting behavior: opening accounts (categorizing an acquisition or expenditure into a mental account), balancing accounts (experiencing satisfaction or discomfort based on whether accounts are in surplus or deficit), and closing accounts (the settlement of an account when a transaction is complete, which is when loss aversion triggers for sunk costs).

The Taxi Driver Study

Camerer, Babcock, Loewenstein, and Thaler (1997) in the Quarterly Journal of Economics examined NYC taxi driver work decisions to test mental accounting in the field. Taxi drivers face genuinely variable demand: some days are high-demand (busy, high-fare), some are low-demand (slow, lower total fares per hour).

A rational optimizer would work longer on high-demand days (when the return per hour is highest) and shorter on low-demand days (when the return per hour is lowest). The researchers found the opposite pattern: drivers tended to quit earlier on high-demand days. Once they had reached their implicit daily income target, they stopped work even though conditions were optimal. On low-demand days, they worked longer to reach the same target.

The mechanism: drivers were mentally accounting by day, not by week or month. Each day was a separate account with a target. Hitting the target closed the account, making additional high-demand hours feel like surplus beyond the goal. Missing the target on a low-demand day meant the account was still open, requiring more hours regardless of efficiency. This is financially suboptimal but psychologically coherent under mental accounting.

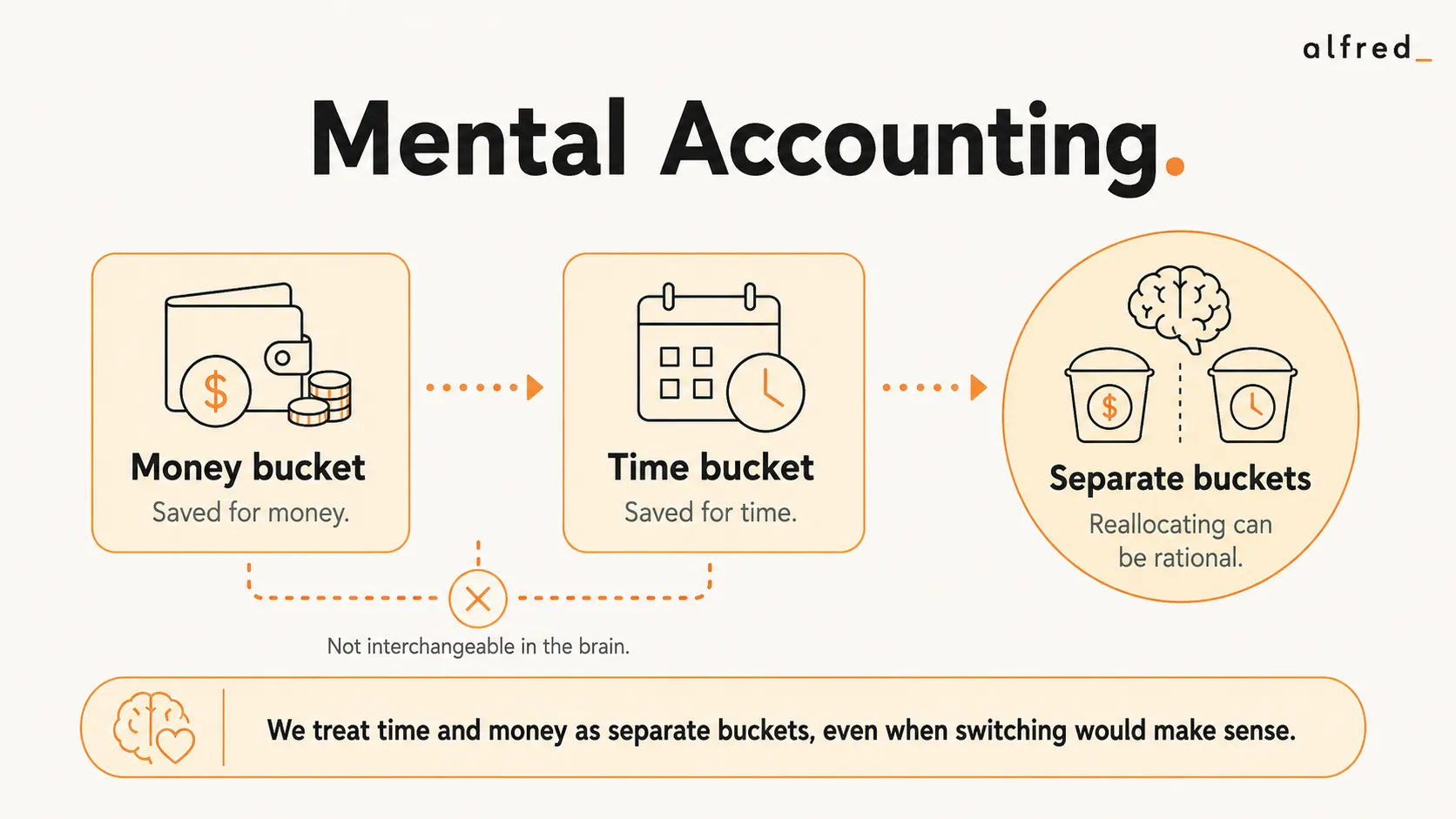

Mental Accounting Applied to Time

The same mechanisms operate for time. Professional time is mentally categorized into accounts that are treated as non-interchangeable: “email time,” “meeting time,” “deep work time,” “admin time.” These mental accounts create psychological barriers to reallocation that don’t exist in purely economic analysis.

- Spillover resistance. A meeting that runs over into “deep work time” is experienced as more costly than the same number of minutes spent in a different part of the day, because it violates a mental account boundary. This explains why people protect certain time blocks with disproportionate energy relative to their objective value.

- Completing small tasks first. Closing a mental account (finishing a simple task) produces satisfaction independent of the task’s actual value. This explains the persistent preference for handling easy emails before difficult strategic work: each completed email closes a small account, producing a stream of small account-closing satisfaction.

- Administrative time as its own category. When administrative tasks are mentally categorized separately from “real work,” there is high psychological resistance to doing administrative work during “real work” time, and high resistance to reducing administrative time even when its actual productivity value is low. The mental account boundary is stickier than the rational allocation would justify.