The Research

Arkes and Blumer published the canonical study in Organizational Behavior and Human Decision Processes (1985). The key scenario: participants were told about a military aircraft program where $9 million had already been spent and the project was behind a competitor’s superior aircraft. Should they continue?

85% vs ~10%

participants who voted to continue the failing military aircraft program: 85% when told $9M had already been spent; only ~10% when no prior investment was mentioned. The sunk cost alone produced a 75-percentage-point difference in the continuation decision.

Arkes & Blumer (1985), Organizational Behavior and Human Decision Processes, 35(1)When prior investment was mentioned, 85% voted to continue the failing program. When no prior investment was mentioned (same future prospects), only approximately 10% chose to continue. The identical future, the same forward-looking calculation, produced dramatically different decisions based purely on what had already been spent.

Their theater ticket field study confirmed the effect in real behavior: full-price season ticket subscribers attended more performances than subscribers who received discounted tickets, despite the cost being identical going forward. The larger sunk cost produced stronger motivation to “get value from” the investment by attending, regardless of whether attending on any given night was actually what the person wanted to do.

Why It Happens: Loss Aversion

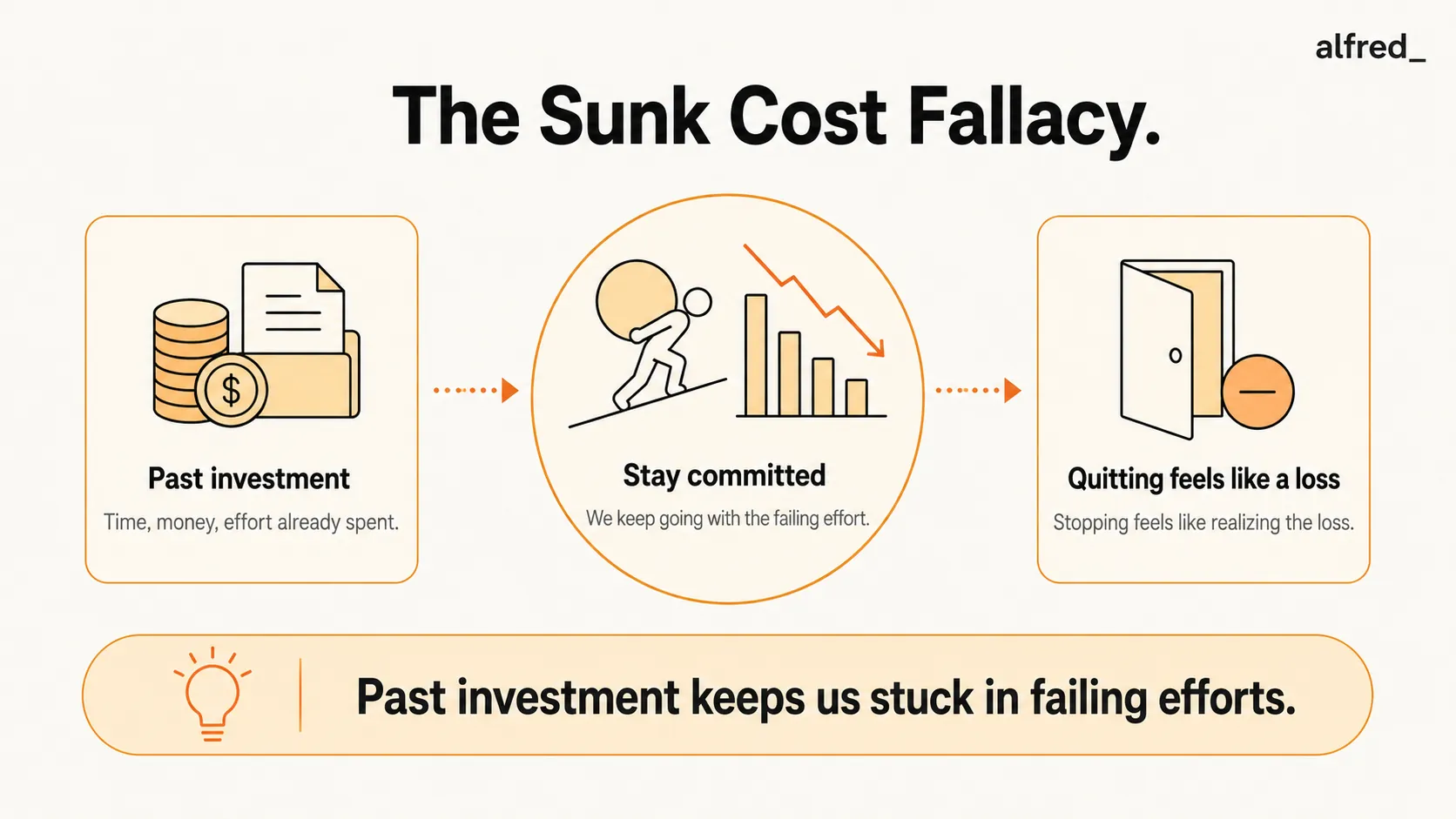

The mechanism is loss aversion, one of the most robust findings in behavioral economics. Kahneman and Tversky’s prospect theory established that losses are weighted approximately twice as heavily as equivalent gains. Abandoning a project converts the investment into a realized loss. Continuing the project keeps the possibility of recovery alive, which means the loss is not yet realized.

This is why sunk cost reasoning is not simply irrational. It feels profoundly rational from the inside. Stopping means admitting the loss. Continuing preserves the possibility, however remote, that the investment was not wasted. The emotional logic is coherent even when the financial logic is not.

Three Executive Sunk Cost Traps

- The failing hire. A significant investment in recruiting, onboarding, and training (6 to 12 months of management time and salary) creates intense sunk cost pressure to “make it work.” The forward-looking question (is this person likely to succeed in this role?) gets contaminated by the backward-looking one (can I justify what was spent?). Organizations frequently keep poor-fit hires longer than rational analysis supports, extending the cost rather than limiting it.

- The legacy vendor. Switching costs are real, but they are future costs, included correctly in a forward-looking analysis. What is incorrectly included is the cost of past contracts: “We’ve spent $2M with them over five years.” That $2M is gone regardless of whether you renew. The renewal decision should be based only on the forward-looking comparison between the incumbent and alternatives.

- The product roadmap past market contradictions. Product investments create some of the most powerful sunk cost dynamics: 18 months of engineering effort, a public announcement, organizational identity attached to the direction. When market signals contradict the approach, the sunk investment creates pressure to persist and to interpret ambiguous signals as confirmation rather than contradiction.

The Clean Diagnostic

The corrective question: “If I had not already made any investment, and someone offered me this opportunity at exactly the current expected cost and return, would I take it?” If yes, continue. If no, the current investment is sunk cost driving the decision.

This question is deceptively simple and practically difficult, because answering it requires actually setting aside the investment, which loss aversion makes viscerally uncomfortable. The question can be useful as a conversation-starter in group settings specifically because it surfaces the sunk cost reasoning explicitly, making it available for examination rather than operating as an invisible thumb on the scale.