Prospect Theory: The Shape of Value

Kahneman and Tversky published “Prospect Theory: An Analysis of Decision Under Risk” in Econometrica in 1979 (Vol. 47, No. 2, pp. 263–291). The paper introduced a descriptive theory of decision-making under uncertainty that accounted for patterns in human choices that expected utility theory could not explain.

The central construct is a psychological value function with three key properties. First, it is defined over changes from a reference point rather than over absolute wealth: what matters is whether you are gaining or losing relative to where you started. Second, it is concave in the gain domain (each additional gain produces less psychological impact than the last) and convex in the loss domain (each additional loss produces less additional pain than the first). Third, and most consequential, it is steeper in the loss domain than in the gain domain: the function descends more sharply for losses than it rises for equivalent gains.

The 1979 paper established this asymmetry qualitatively through a series of choice problems, specifically hypothetical gambles showing that people’s choices were systematically inconsistent with expected utility maximization in ways that the S-shaped value function predicts. But the original paper did not estimate a specific numerical coefficient for the loss aversion asymmetry.

The Loss Aversion Coefficient: Lambda = 2.25

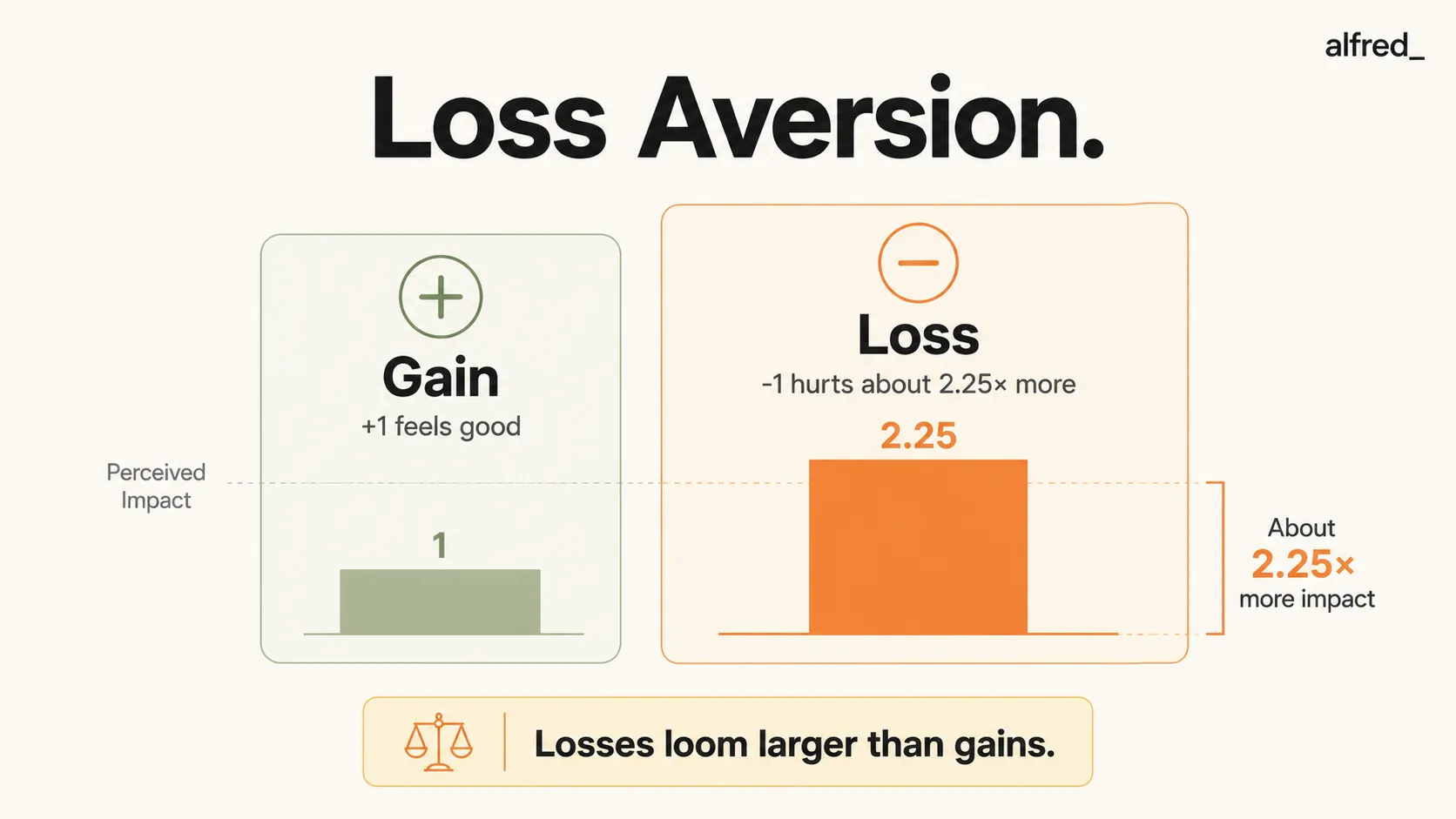

The specific quantification of loss aversion came thirteen years later. Tversky and Kahneman published “Advances in Prospect Theory: Cumulative Representation of Uncertainty” in the Journal of Risk and Uncertainty in 1992 (Vol. 5, pp. 297–323). This paper developed cumulative prospect theory, a mathematically refined version of the 1979 framework, and estimated the key parameters empirically.

The loss aversion parameter lambda was estimated at 2.25. This means that in the median empirical study, losses are weighted approximately 2.25 times more heavily than equivalent gains in the value function. The popular shorthand, “losses feel about twice as painful as gains feel good,” is an approximation of this 1992 estimate, and it technically slightly understates the finding.

It is important to note that lambda = 2.25 is a population-average estimate; individual loss aversion coefficients vary, and the degree of loss aversion depends on the stakes, domain, and how the reference point is framed. But the directional finding, that losses outweigh equivalent gains, has replicated across cultures, stakes levels, and decision domains.

Professional Consequences

- Negotiation framing. The same outcome framed as a gain versus a loss produces different levels of acceptance. Framing a concession as “avoiding a loss” rather than “achieving a gain” makes it psychologically heavier. This is why contract negotiations often produce more movement when parties emphasize what they will lose from a deal not closing than what they will gain from closing it.

- Change management. Organizational change initiatives consistently encounter more resistance than their objectively expected benefits would predict. Loss aversion explains why: employees weight the concrete losses of familiar processes, relationships, and roles approximately 2x relative to the abstract gains of the new state. Change communications that acknowledge specific losses and provide credible substitutes outperform communications that enumerate only the gains.

- The endowment effect. People value objects they own more than identical objects they don’t own, because giving up an owned object registers as a loss. This is why sellers’ reservation prices consistently exceed buyers’ maximum willingness to pay for the same item. In internal resource allocation, the same effect makes it harder to reallocate headcount, budget, and tools from incumbent owners than it would be to allocate them fresh.

- Holding losing positions too long. Loss aversion creates a tendency to hold investments, projects, and strategies beyond their rational stopping point because realizing a loss makes it concrete. Unrealized losses can be ignored; realized losses cannot. This is sunk cost and loss aversion in combination: the mechanism that keeps failing projects alive and prevents portfolio rebalancing.