How Hyperbolic Discounting Creates Time Inconsistency

Standard economic models assume exponential discounting: a reward delayed by one day is worth a fixed proportion less than the immediate reward, and this proportion is constant regardless of when the delay occurs. Under exponential discounting, if you prefer $110 in 31 days to $100 in 30 days (you’re willing to wait one more day for $10), you will also prefer $110 tomorrow to $100 today.

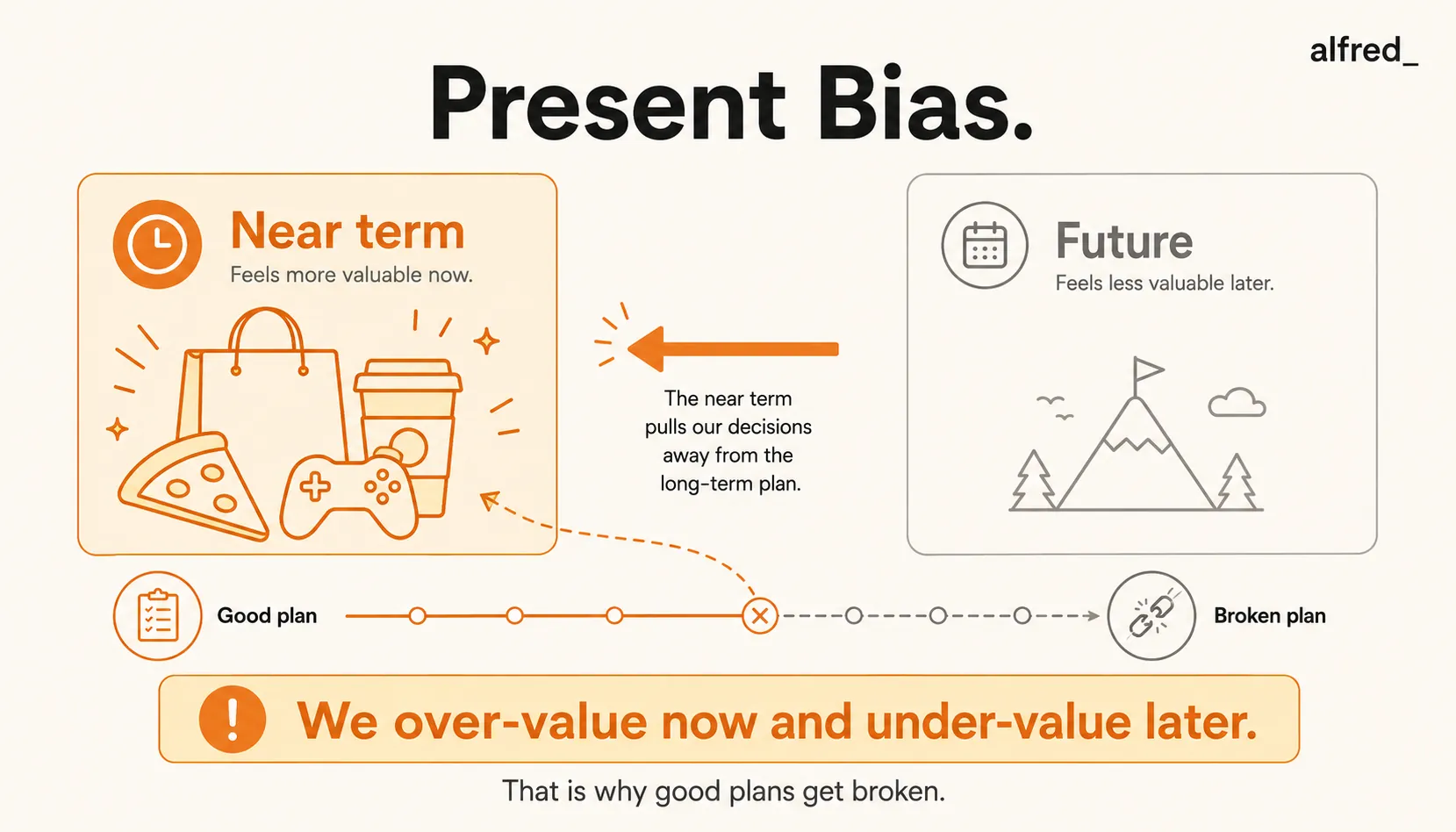

Humans don’t discount this way. The empirical finding, documented across multiple experimental paradigms and real-world behaviors by researchers including George Ainslie and Richard Thaler from the 1970s onward, is that people discount the immediate present much more steeply than equivalent delays further in the future. The discount rate between now and one hour from now is higher than the discount rate between next month and next month plus one hour.

This hyperbolic shape of the discount function creates time inconsistency: preferences that are rational from a future vantage point become irrational when the decision point arrives. You genuinely prefer $110 in 31 days to $100 in 30 days when both are in the future. But when day 30 arrives, the $100 that is now immediate is weighed against $110 that is now one day away, and many people switch their preference to take the $100 now. The preference reversal happens not because new information arrived, but because proximity to the present inflates the immediate option’s value.

Laibson’s Model

David Laibson published “Golden Eggs and Hyperbolic Discounting” in the Quarterly Journal of Economics in 1997 (Vol. 112, No. 2, pp. 443–478). The paper is primarily a theoretical and macroeconomic contribution. It is not an experimental study of individual choice but a formal economic model.

Laibson used a quasi-hyperbolic (beta-delta) discounting specification: immediate payoffs are discounted by a factor beta (which captures present bias, the extra weight on immediate versus all future rewards), and all future payoffs are discounted at the standard exponential rate delta. When beta is less than 1 (present bias is present), the model predicts time-inconsistent preferences.

The paper’s central application was household savings behavior. Standard exponential discounting models predicted that households would smooth consumption over time, saving when young to spend when old. Actual household savings rates were far below model predictions. Laibson’s model showed that present-biased households would systematically under-save: each period, the immediate consumption option is inflated relative to future savings, producing persistent under-saving even among households that intend to save. He also showed that illiquid assets (mortgages, retirement accounts, commitment savings) function as self-imposed commitment devices precisely because they remove the ability to yield to present bias.

Professional Consequences and Solutions

- Project scheduling and deadline management. Present bias predicts that work scheduled for the future will be consistently underestimated in difficulty at the time of scheduling and overestimated in available time. The result is calendars systematically over-committed in the future and under-executed in the present. The structural solution is to treat future calendar commitments with the same scrutiny as immediate commitments: if you wouldn’t agree to this meeting tomorrow, don’t agree to it next week.

- Commitment to development and learning. Professional development investments (reading, training, skill-building) involve costs that are immediate (time, effort now) and benefits that are delayed (capability months from now). Present bias systematically underweights the future benefit relative to the immediate cost, producing chronic under-investment in development at every decision point. External commitments (cohort programs, scheduled sessions, peer accountability) convert the future into a present by making the immediate cost of not developing visible and socially concrete.

- Decision timing. Decisions about future commitments are made from a future vantage point that will be subject to present bias when the commitment arrives. This means that optimal commitments, the ones you’d make if you had consistent preferences, should account for the preference reversal that will occur when the time arrives. Commitment devices, advance scheduling, and pre-commitment to decision rules are mechanisms that transfer the rational far-future preference into a present-moment constraint that survives the arrival of the decision point.