Weinstein’s 1980 Study

Neil Weinstein published “Unrealistic optimism about future life events” in the Journal of Personality and Social Psychology in 1980 (39(5), 806–820). The study asked university students to estimate their own likelihood of experiencing 42 life events (18 positive and 24 negative) relative to the average student at their university.

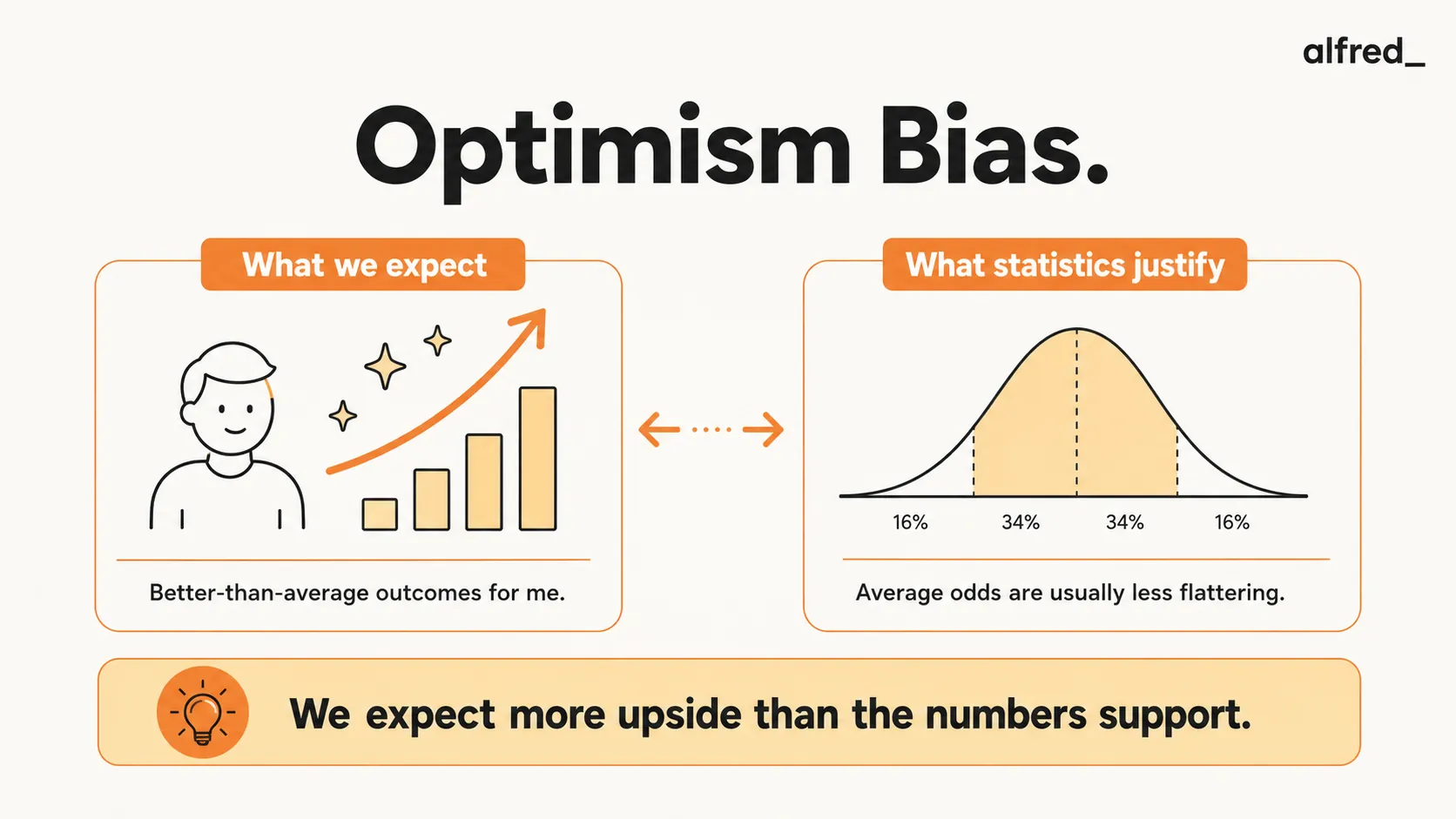

A well-calibrated population would show that the average self-assessment matches the population average; by definition, half of people should be above average and half below. What Weinstein found was systematic divergence: participants rated themselves as more likely than average to experience positive events (good job offer, travel, home ownership) and less likely than average to experience negative ones (divorce, illness, job loss, accident). Since most people cannot simultaneously be above average on positive outcomes and below average on negative ones, this represents a systematic bias rather than accurate self-knowledge.

Systematic, not random

Weinstein found that across both positive events (rated more likely than average for self) and negative events (rated less likely than average for self), participants showed optimistic bias. This was strongest for controllable events and events perceived as rare, conditions where base rate information was least available.

Weinstein, N.D. (1980). Journal of Personality and Social Psychology, 39(5), 806–820.Weinstein identified several moderators: the bias was stronger for events the person felt they had some control over (controllability makes it feel like the negative event can be avoided) and for events perceived as relatively rare (low base rates are easier to discount than common ones). The bias was weaker for events that had already happened to someone close to the participant, which made the base rate more personally salient.

The Neural Mechanism: Asymmetric Belief Updating

Tali Sharot and colleagues identified a neural basis for optimism bias in their 2011 research (Nature Neuroscience, 14(11), 1475–1479). Participants received information about their relative risk for various negative life events, sometimes better and sometimes worse than they had expected. Brain imaging during this task showed that the inferior frontal gyrus encoded prediction errors differently for better-than-expected information versus worse-than-expected information.

When information was more optimistic than the participant’s prior estimate, belief updating was more complete: the participant revised their estimate more strongly in the direction of the better news. When information was more pessimistic than expected, belief updating was weaker: the participant partially discounted the worse news. This asymmetric updating produces optimism bias as a cumulative result: over many rounds of information, beliefs drift upward because good news is weighted more heavily than bad news of equal magnitude.

Professional Consequences

- Project planning and risk assessment. Optimism bias is a primary driver of the planning fallacy: projects are estimated to take less time and cost less than they actually do because planners focus on their plan’s most likely scenario (a success scenario) and underweight the realistic probability of delays, setbacks, and rework. Reference class forecasting, which explicitly anchors estimates to the historical distribution for comparable projects, is the main evidence-based corrective, because it forces exposure to base rates that optimism bias would otherwise discount.

- New venture and product decisions. Optimism bias is structurally elevated in entrepreneurial and new-product contexts because the control dimension that Weinstein identified is high (“I can make this succeed”), the base rate is often unknown or discounted, and the founders’ intense engagement with the best-case scenario makes it cognitively more available. Pre-mortem analysis, which explicitly generates the scenario in which the venture has failed, partially counteracts this by making the pessimistic scenario as vivid and concrete as the optimistic one.

- Updating from negative feedback. The asymmetric updating mechanism predicts that individuals will be slower to update their expectations downward after bad performance data than upward after good data. Teams that perform above forecast raise estimates strongly; teams that perform below forecast revise less than the data warrants. This asymmetry compounds over time into systematic optimism that compounds at each forecast revision.